Debt Snowball vs. Debt Avalanche: Which Strategy Will Get You Debt-Free Faster?

Compare the two most powerful debt payoff methods: Snowball (focusing on psychology) and Avalanche (focusing on math). Find out which strategy saves you the most money and which keeps you motivated to reach zero debt.

11/18/20252 min read

You have built your budget, secured your emergency fund, and started investing for your future. The last hurdle blocking your path to financial freedom is debt.

While you know you need to pay it off, the real struggle is finding a system that keeps you motivated and ensures your money is working as hard as possible.

For decades, two strategies have dominated the debt payoff landscape: the Debt Snowball and the Debt Avalanche. Both are incredibly effective, but they target different goals. One saves you the most money, and the other saves your sanity.

At FinScopeHub, we believe the best strategy is the one you actually stick to. Here is the definitive breakdown of both methods so you can choose the one that aligns with your financial personality.

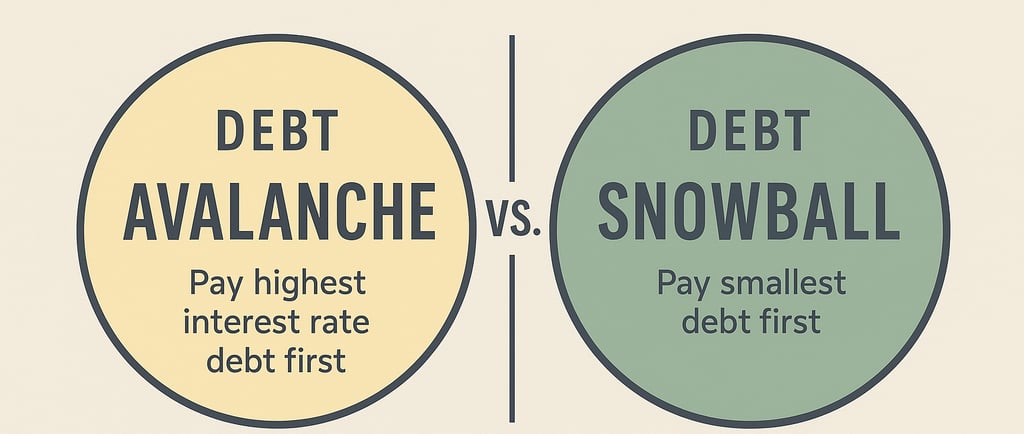

Method 1: The Debt Avalanche (Math Wins)

The Debt Avalanche method is the mathematically superior choice. It is designed to save you the maximum amount of money and pay off your debt in the shortest amount of time possible.

How It Works:

List all your debts (credit cards, loans, etc.) from highest interest rate to lowest interest rate. Ignore the balance size.

Make minimum payments on every debt except the one with the highest interest rate.

Throw every extra dollar you can find at that highest-interest debt until it is gone.

Once the first debt is gone, take the money you were paying on it and apply it to the debt with the next highest interest rate.

The Pros and Cons:

Pro: Saves the most money on interest, guaranteeing the shortest path to debt freedom.

Con: It can take a long time to knock out the first few debts, especially if your highest-interest debt also has a large balance, which can be psychologically draining.

Method 2: The Debt Snowball (Psychology Wins)

The Debt Snowball method prioritizes behavior and motivation over pure math. It was popularized by financial guru Dave Ramsey and is beloved by people who need quick wins to stay on track.

How It Works:

List all your debts from smallest balance to largest balance. Ignore the interest rate.

Make minimum payments on every debt except the one with the smallest balance.

Throw every extra dollar you can find at that smallest-balance debt until it is gone.

Once the first (smallest) debt is gone, you celebrate! Then, take the money you were paying on it and apply it to the debt with the next smallest balance. The payment amount snowballs, creating momentum.

The Pros and Cons:

Pro: Provides immediate, powerful psychological wins. Seeing a debt completely disappear provides the necessary fuel to stick with the plan long-term.

Con: You will ultimately pay more interest because you are prioritizing balance size over interest rate.

The Final Verdict: Which Strategy Is Right For You?

The choice is simple:

Choose the Debt Avalanche if: You are disciplined, motivated by saving money, and can stick to a long-term plan without needing frequent small victories. You value math over momentum.

Choose the Debt Snowball if: You get easily discouraged, need quick wins to stay motivated, and often struggle to adhere to financial plans. You value momentum over math.

The difference in total interest paid between the two methods is usually less than the cost of quitting the plan entirely. The best plan is the one that gets you to zero debt, period.

FinScopeHub's Advice: If you are unsure, try the Debt Snowball first. Getting rid of that first balance provides a dopamine hit that can create a lifelong financial habit. Once you have momentum, you'll be unstoppable.